Executive Briefing

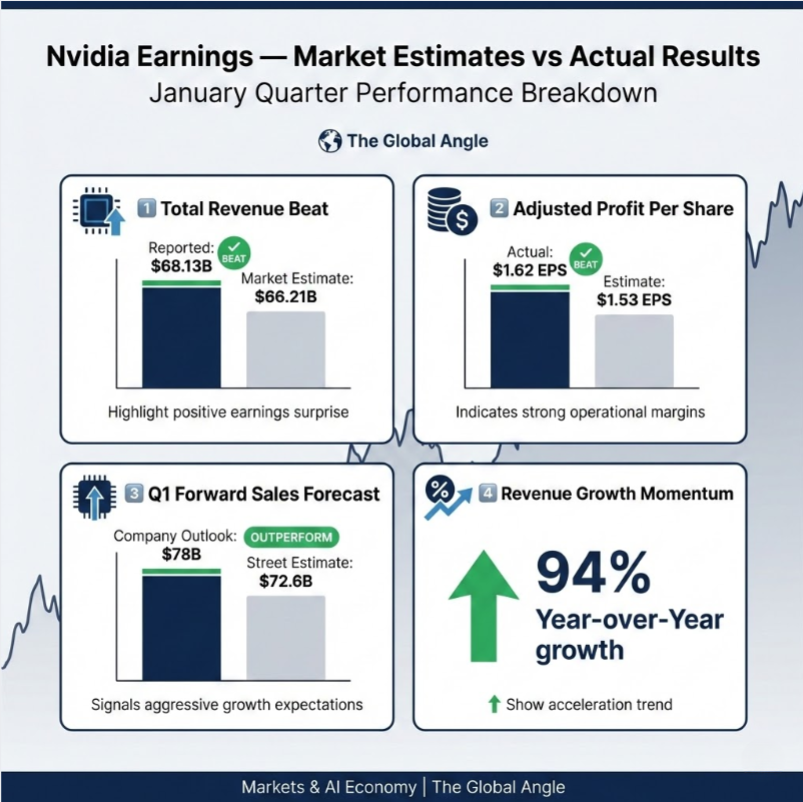

- The Core Event: Nvidia Q1 Earnings reported a massive 94% revenue jump for the January quarter, hitting $68.13 billion and beating Wall Street’s lofty expectations.

- The Primary Data Point: Big Tech “Hyperscalers” (like Meta and Google) are projected to spend a staggering $630 billion on AI infrastructure in 2026, keeping demand for Nvidia chips at record highs.

- The Hidden Market Impact: Despite the “beat,” Nvidia’s stock remained flat as investors began questioning the company’s “cash hoard”—nearly $100 billion—and demanding more direct returns through dividends or buybacks.

Nvidia, the world’s most valuable company, just proved that the AI boom isn’t over yet. However, for the first time in 14 quarters, “good” might not be good enough for a spoiled Wall Street.

According to Nvidia’s Q1 earnings for 2026, the company forecast sales of $78 billion for the coming quarter, easily topping the $72.6 billion analysts expected.

But even with these blockbuster numbers, the stock didn’t budge. Why? Investors are no longer just looking at sales—they want to see the cash.

The $100 Billion Question: Where is the Cash Going?

Nvidia is currently a money-printing machine. Analysts estimate the company will generate roughly $100 billion in cash this year alone.

During the earnings call, analysts pressed executives on why that money isn’t being handed back to shareholders. Nvidia CFO Colette Kress remained firm: the company plans to keep re-investing every cent into the “AI ecosystem” to stay ahead of the pack.

Nvidia Q1 Earnings Report

| Financial Metric | Reported (Jan Quarter) | Market Estimate |

| Total Revenue | $68.13 Billion | $66.21 Billion |

| Adjusted Profit | $1.62 per share | $1.53 per share |

| Q1 Sales Forecast | $78 Billion | $72.6 Billion |

| Revenue Growth | 94% Year-over-Year | N/A |

CEO Jensen Huang argued that we are seeing a fundamental shift in how computing works. He believes the world is moving away from traditional software to AI-generated output, requiring a massive, permanent increase in global data centre capacity.

The Rise of the “In-House” Threat

While Nvidia dominates the market today, its biggest customers are becoming its biggest rivals.

Tech giants like Meta, Google, and Amazon are tired of waiting for Nvidia’s expensive chips. They are now designing their own “in-house” processors (like Google’s TPUs) to power their data centres.

Nvidia’s sales are also becoming dangerously concentrated. Just two secret customers now account for 36% of all Nvidia’s sales. If one of these giants decides their in-house chips are “good enough,” Nvidia’s revenue could take a massive hit.

The Competitive Landscape in 2026

| Competitor | Strategy | Current Status |

| AMD | Releasing new flagship AI servers. | Already winning deals with Meta. |

| Using in-house TPUs for Claude & Meta. | Emerging as the top “Silicon” rival. | |

| Meta | $630B total CapEx for 2026. | Splitting spend between Nvidia and in-house. |

The China Factor and Export Curbs

One major cloud hanging over Nvidia is China. For a long time, U.S. export curbs meant Nvidia couldn’t sell its best chips to the massive Chinese market.

There is a small glimmer of hope, though. Nvidia recently received licenses from the U.S. government to ship “small amounts” of its H200 chips to China. While this isn’t a total return to normal, it shows that the government is willing to let some high-end tech through the cracks.

Meanwhile, rival AMD has already started including China sales back into its financial forecasts, potentially giving them a head start in the region.

What This Means for the Future

Nvidia is essentially a victim of its own success. When you grow 94% in a single year, people stop being impressed by “normal” growth.

The company has secured enough capacity from its manufacturer, TSMC, to meet demand for the next few quarters. However, the battle for top AI engineers is driving up “stock-based compensation” costs. To keep the best minds from moving to OpenAI or Google, Nvidia has to pay out billions in company shares.

The next few months will decide if Nvidia can remain the king of AI, or if the “Hyperscalers” will successfully build their own empires without them.

Frequently Asked Questions

Why did Nvidia’s stock stay flat after beating estimates?

Investors had already “priced in” a win. After 14 quarters of beating estimates, Wall Street was looking for something extraordinary—specifically, a plan to return some of Nvidia’s $100 billion cash pile to shareholders through dividends.

Is there an AI slowdown happening?

According to the latest data, no. Big Tech firms are planning to spend over $630 billion on AI infrastructure in 2026. However, Nvidia faces more competition now from AMD and in-house chips developed by Google and Meta.

ALSO READ: The New $31 Counterstrike: Paramount Warner Bros Discovery merger, Is Netflix Losing the Deal?

ALSO READ: China FTA loopholes 2026: How China Outsmart’s Global Tariffs With The “Made in Anywhere” Strategy

The Complete History of Iran Israel Relations: From Secret Allies to Arch-Rivals

Executive Briefing The Dramatic Shift: Today, Iran and Israel are engaged in a sprawling, multi-front…

Russian vs Gulf Crude Oil: Price, Refining, and Efficiency Compared

Executive Briefing Two of the most heavily traded categories in the world are Russian vs…

Who is Winning the US Iran War 2026? Casualties, Costs, and the 2026 Timeline

Executive Briefing (Update: March 12, 2026) As the 2026 Middle East conflict reshapes the global…

Global Oil Price Hike 2026: Petrol Prices & Strategic Reserves by Country

Executive Briefing Global Oil Price Hike 2026 (Update: March 12, 2026) The Price Shock: Following…

Can Trump Be Impeached In Midterm Elections 2026? Odds, Stats, and the Process Explained

Executive Briefing (Update: March 2026) As the United States gears up for the pivotal 2026…

Who Was Arrested From the Epstein Files in 2026? Photos & Facts

Executive Briefing (Update: March 2026) If you are wondering exactly who was arrested from the…

Ibrahim is the Founder and Lead Analyst at The Global Angle, an independent digital platform dedicated to factual geopolitical analysis and international affairs. Based in India, he combines an engineering background with a deep focus on global markets, diplomacy, and strategic security. Ibrahim leverages a data-driven, analytical approach to break down complex international conflicts and economic shifts, helping readers see beyond standard news narratives. When he isn’t researching global policy, he focuses on digital publishing, search engine optimization, and platform architecture.