IMF economic forecast: IMF Warns Growth Slows in 2026 as War, Inflation and Trade Fragmentation Rises

The International Monetary Fund’s April 2026 World Economic Outlook signals a weaker global growth environment as geopolitical conflict, trade fragmentation, and persistent inflation continue to pressure the world economy.

Ongoing instability in the Middle East and Eastern Europe has increased uncertainty across energy markets, shipping routes, and investment flows. While the global economy is not in immediate crisis, the IMF outlook suggests that growth is becoming more fragile and uneven.

This is not simply a short-term slowdown. It reflects deeper structural changes in how countries trade, invest, and manage economic risk.

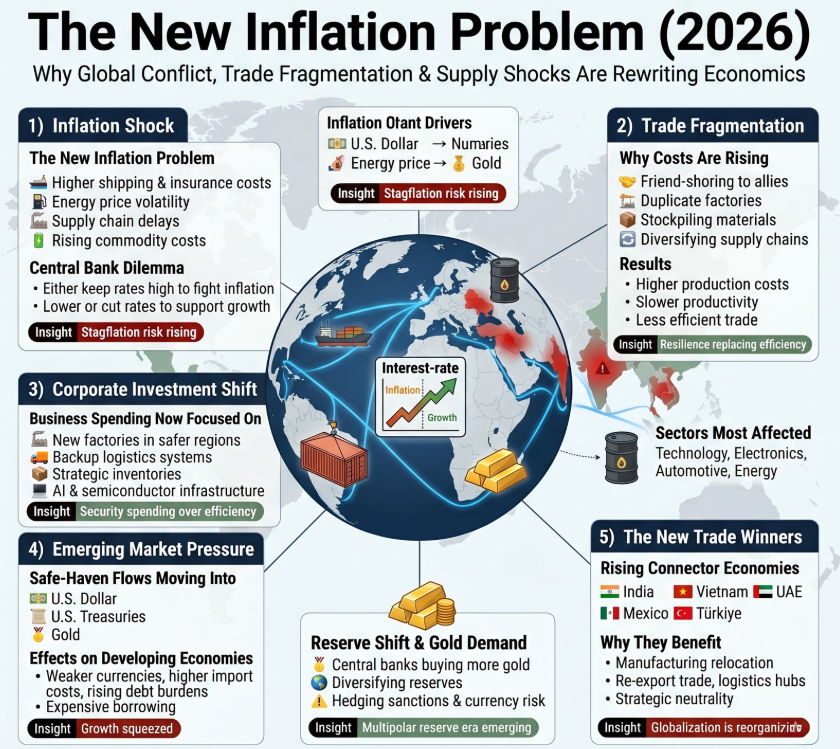

The New Inflation Problem: Supply Shocks, Not Excess Demand

Inflation in 2026 remains elevated in many regions, but the causes are different from earlier post-pandemic demand surges.

Recent price pressure has been driven by:

- Higher shipping and insurance costs due to maritime disruptions

- Energy price volatility linked to regional conflict

- Supply chain delays in key industrial sectors

- Rising costs of strategic commodities

This creates a difficult challenge for central banks.

Interest rate hikes are effective when inflation is caused by excess borrowing or overheated consumer demand. But monetary policy cannot reopen blocked shipping lanes or restore damaged energy infrastructure.

As a result, many central banks face a difficult balance:

- Keep rates high to contain inflation

- Or cut rates to support slowing growth

That combination of sticky prices and weak growth raises concerns about a stagflation-like environment in some economies.

Trade Fragmentation Is Raising Long-Term Costs

The IMF has repeatedly warned about growing geoeconomic fragmentation.

Countries are increasingly reorganizing supply chains around political alliances, security concerns, and strategic resilience rather than lowest-cost efficiency.

This shift includes:

- Friend-shoring production to allied nations

- Diversifying away from single-country dependence

- Building duplicate manufacturing capacity

- Stockpiling critical materials

These strategies may improve national security, but they also come with economic costs.

For decades, globalization helped lower prices by concentrating production where it was cheapest and most efficient. In contrast, the new model prioritizes resilience over efficiency.

That likely means:

- Higher production costs

- More expensive consumer goods

- Slower productivity gains

- Reduced trade efficiency

Corporate Investment Is Changing

A growing share of business investment is now going toward resilience rather than pure innovation.

Instead of focusing only on research, software, or expansion, many firms are spending heavily on:

- New factories in politically safer regions

- Redundant logistics systems

- Strategic inventory reserves

- Semiconductor and AI infrastructure

Some of this spending may generate long-term returns. However, it can also reduce short-term efficiency and delay profitability.

This is especially visible in sectors such as:

- Technology

- Electronics

- Automotive manufacturing

- Energy systems

Emerging Markets Face Stronger Pressure

Global conflict and uncertainty often trigger capital flows into safe-haven assets such as:

- U.S. Dollar

- U.S. Treasury bonds

- Gold

When this happens, many developing economies face additional strain.

Common effects include:

- Weaker local currencies

- Higher import costs

- Rising debt-servicing burdens

- More expensive borrowing

This is particularly serious where governments or companies hold large amounts of U.S. dollar-denominated debt.

To defend their currencies, some emerging market central banks may keep interest rates high even when domestic growth is weak.

That can slow investment, employment, and household demand.

A New Global Trade Map Is Emerging

Trade fragmentation does not necessarily reduce trade overall. Often, it reroutes trade through intermediary economies.

Countries such as:

- India

- Vietnam

- Mexico

- UAE

- Türkiye

have become increasingly important as connectors in global supply chains.

They benefit from:

- Manufacturing relocation

- Re-export trade

- New logistics hubs

- Strategic neutrality

This suggests the global economy is not deglobalizing completely—it is reorganizing.

Why Gold and Reserve Diversification Matter

Another visible trend is central bank diversification away from excessive reliance on a single reserve asset.

Many countries have increased gold purchases while also seeking broader reserve strategies.

Drivers include:

- Sanctions risk

- Currency volatility

- Desire for reserve diversification

- Long-term geopolitical uncertainty

This does not mean the U.S. dollar is losing dominance immediately, but it does indicate a more cautious and multipolar reserve environment.

What the IMF Outlook Really Signals

The April 2026 outlook points to three major realities:

Growth is slowing

Global expansion continues, but at a weaker pace.

Inflation may remain sticky

Especially where supply disruptions continue.

Fragmentation has economic costs

Security-driven economics is replacing pure efficiency.

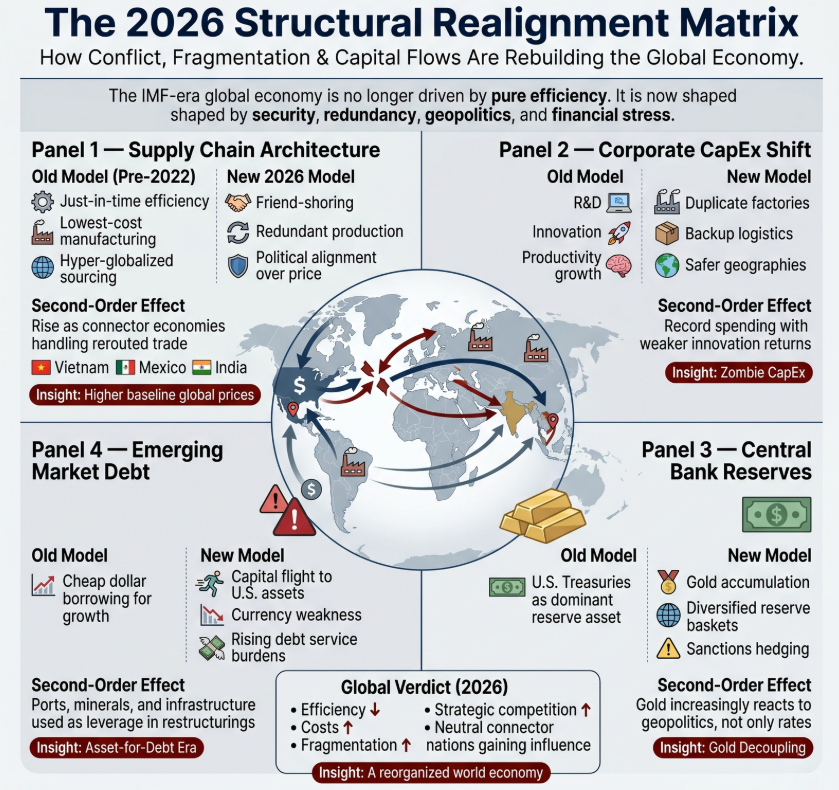

The 2026 Structural Realignment Matrix

| Economic Vector | The Old Paradigm (Pre-2022) | The New Reality (2026 IMF Projection) | Information Gain: The Second-Order Effect |

| Supply Chain Architecture | “Just-in-Time” efficiency; optimization for the absolute lowest manufacturing cost. | “Friend-shoring”; forced redundancy and political alignment over price. | The Connector Economy Tollbooth: Nations like Vietnam, Mexico, and India act as mandatory middle-men, washing Chinese goods for Western markets. They extract massive fees, permanently raising baseline retail prices globally. |

| Corporate CapEx (Capital Expenditure) | Billions invested into R&D, software innovation, and technological breakthroughs. | Billions diverted to build duplicate, redundant factories in politically safe zones. | Zombie CapEx: Corporations are spending record amounts of capital that generates zero new innovation. Global technological productivity growth is actively stalling because money is spent on geography, not discovery. |

| Central Bank Reserves | Global reliance on U.S. Treasuries as the ultimate, neutral safe-haven asset. | Aggressive diversification away from the U.S. Dollar to hedge against sanction exposure. | The Gold Decoupling: Emerging market central banks are hoarding physical gold at record rates. Gold has structurally decoupled from real interest rates, acting now as a geopolitical fear index rather than a standard inflation hedge. |

| Emerging Market Debt | Developing nations borrow cheap U.S. Dollars to fund domestic infrastructure growth. | Capital flight to the U.S. forces EM currencies down and explodes their debt servicing costs. | Asset-for-Debt Swaps: Facing sovereign default, vulnerable nations are being forced to surrender strategic physical assets (deep-water ports, critical mineral mines) to non-Western creditors in lieu of dollar payments. |

What Could Improve the Outlook?

Several developments could improve conditions:

- De-escalation in major conflict zones

- Stabilization in oil and gas prices

- Lower shipping disruptions

- Gradual interest rate cuts

- More stable trade relations

If these occur, growth could recover faster than expected.

Conclusion

The world economy in 2026 is not collapsing, but it is changing.

The era of frictionless globalization, ultra-cheap supply chains, and low geopolitical risk appears to be fading. In its place is a more complex system shaped by security concerns, strategic competition, and persistent inflation risks.

For businesses, governments, and investors, the key challenge is no longer maximizing efficiency alone—it is adapting to a world where resilience has become just as valuable.

Sources

IMF – World Economic Outlook April 2026

OECD – Trade and Fragmentation Reports

World Bank – Commodity Markets Outlook

BIS – Emerging Market Dollar Debt Studies

Reuters – Global inflation, conflict and trade coverage

What is the primary conclusion of the IMF’s April 2026 World Economic Outlook?

The IMF warns that expanding global conflicts, specifically in the Middle East and Europe, are actively restricting global economic growth and engineering an environment of persistent high inflation.

Why is inflation remaining high despite central bank interventions?

The current inflation spike is driven by supply-side pressures. Maritime shipping disruptions and unstable energy prices limit the supply of goods. This prevents central banks from executing anticipated interest rate cuts, as monetary policy cannot solve physical supply chain blockades.

What does the IMF mean by the world economy “splitting up”?

The global economy is fracturing into politically aligned economic blocs. While this strategy reduces national security vulnerabilities, it destroys manufacturing efficiency. Rebuilding redundant supply chains in allied nations makes global trade structurally more expensive.

How are emerging markets reacting to the 2026 geopolitical climate?

Developing nations are facing severe economic strain. Institutional capital is abandoning emerging markets in favor of safer, developed economies. This capital flight leaves developing countries with rapidly depreciating currencies and unsustainable sovereign borrowing costs.

ALSO READ: Global Debt Report 2026 Analysis and the $348 Trillion World Debt Crisis

Russia China trade relations 2026: Sanctions Evasion, Dual-Use Tech, and the Putin-Xi Summit

Russia China trade relations 2026: Sanctions Evasion, Dual-Use Tech, and the Putin-Xi Summit Executive Briefing…

What is Hantavirus Outbreak 2026: Symptoms, Vaccine Status, and the Climate Vector

What is Hantavirus Outbreak 2026: Symptoms, Vaccine Status, and the Climate Vector The Immediate Trigger:…

Starlink & SpaceX IPO 2026: Everything You Need to Know

Starlink & SpaceX IPO 2026: Everything You Need to Know The Valuation: According to Institutional…

What is OPEC? How the Oil Cartel Functions and Why It’s Fracturing in 2026

What is OPEC? How the Oil Cartel Functions and Why It’s Fracturing in 2026 The…

Why the UAE Quit OPEC and the Birth of the Petro-Rupee

Why the UAE Quit OPEC and the Birth of the Petro-Rupee The Rupture: The United…

Microsoft OpenAI Partnership Ends: Why Microsoft is Dropping OpenAI’s Exclusive License

Microsoft OpenAI Partnership Ends: Why Microsoft is Dropping OpenAI’s Exclusive License The Announcement: On April…

Ibrahim is the Founder and Lead Analyst at The Global Angle, an independent digital platform dedicated to factual geopolitical analysis and international affairs. Based in India, he combines an engineering background with a deep focus on global markets, diplomacy, and strategic security. Ibrahim leverages a data-driven, analytical approach to break down complex international conflicts and economic shifts, helping readers see beyond standard news narratives. When he isn’t researching global policy, he focuses on digital publishing, search engine optimization, and platform architecture.